What to Do with Life Insurance Policies After a Divorce

When someone decides to take out a life insurance policy, he or she usually does so to protect his or her spouse, children, and other dependants in the event of the person’s death. However, when spouses separate in a divorce, those life insurance policies and their beneficiaries get thrown into question, especially when one or both ex-spouses remarry. Questions arise, such as: Who should take out or pay for a policy? Who should be the beneficiaries? Is the policy a marital asset?

The policy owner and the insured can be the same person or different people, but we will emphasize again that only the policy owner can name the beneficiaries and make payments to the insurance company.

What Happens to the Policy After a Divorce?

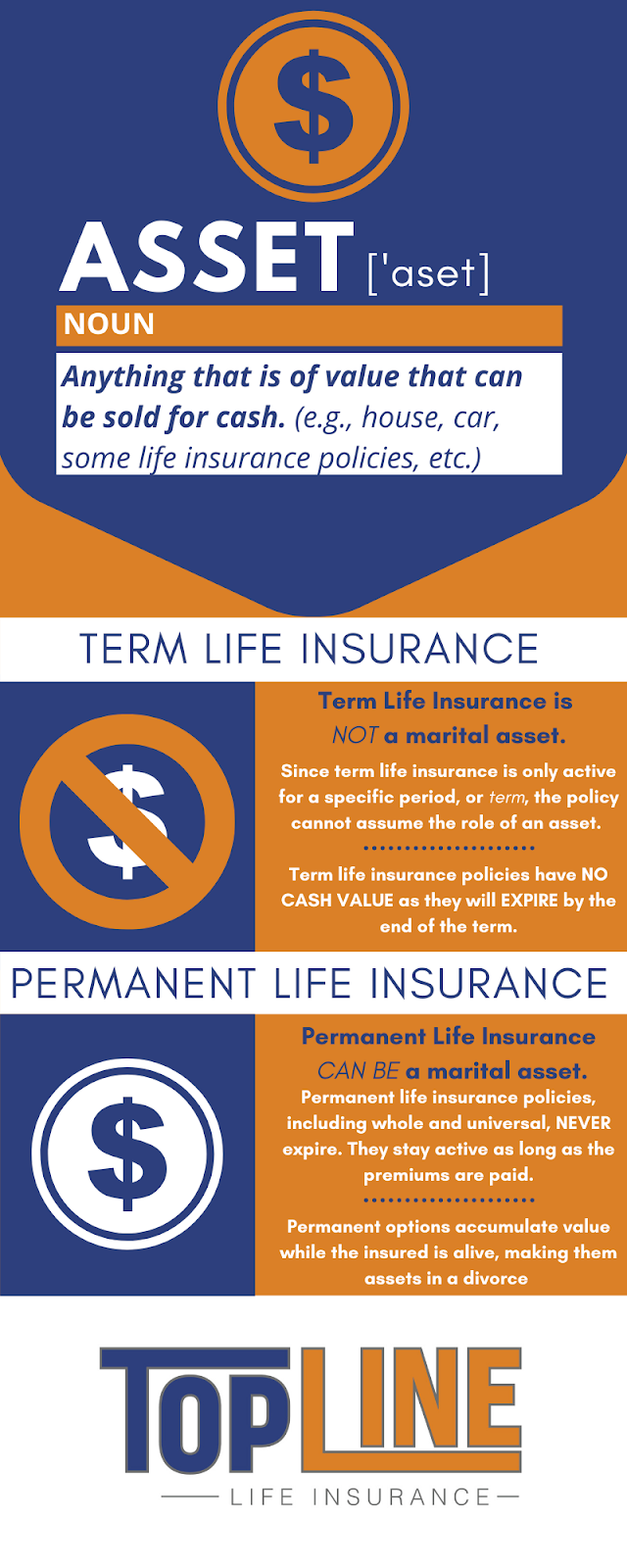

Initially, when a couple divorces, absolutely nothing changes. Since life insurance is a contract between the policy owner and the insurer, if the owner does not change anything on the policy, the policy does not change, including the beneficiaries. The policy owner can make changes, including designating new beneficiaries or having the death benefit go to the insured’s estate to be divvied out in accordance with the insured’s will. While this seems pretty cut and dried, the legal proceedings and divorce settlements can complicate the matter.

In amicable divorces, ex-spouses frequently leave their life insurance plans alone, but many divorces are not so friendly or as simple, which can lead to disputes between exes. Many policy owners do not want to leave their exes as beneficiaries, instead wishing to take the exes off the plans and list their new spouses as beneficiaries or leave their children or other dependants with a larger piece of the death benefit.

These disputes should be handled in court, where a settlement will be agreed upon. Financial obligations like alimony, child support, asset distribution, and other issues brought up in the divorce settlement will also be handled in court.

Is a Life Insurance Policy a Marital Asset?

Find out more about life insurance policies, and speak to a professional insurance broker by calling TopLine Life Insurance today!

Right Here, Right Now.

Your family’s financial safety net is only a few clicks away. Fill out this quick form and get a life insurance quote from TopLine in seconds.

There are many life insurance policies from which to choose, and the best one for you might not be the best for someone else. If you need lower premiums, a term life insurance policy might be a good option. If you are looking for insurance that provides investment opportunities and does not expire until you pass away, a universal plan is an excellent choice. Speak to a TopLine Life Insurance broker to discuss your options.

A life insurance premium is a regular payment you must make to your insurance company to pay for your life insurance policy. Continuous payments will keep your plan active, while missing payments could cause it to lapse. Different policies have different requirements for premium payments, so research possible policies and contact us at TopLine to find the right plan for you.

This answer differs from person to person and is mostly dependant upon your finances. Typically, your minimum amount should be enough to cover your mortgage, loans, credit cards, and any other outstanding payments and debts.

Other considerations include:

- College tuition assistance for your children or grandchildren

- Income replacement for your spouse

- Estate planning

Speak with a TopLine life insurance broker to avoid over or under-insuring yourself.

Generally speaking, buying a life insurance policy when you are younger and healthier gives you a better chance of locking in a favorable policy premium. By purchasing a plan now, you can guarantee your “insurability” for the future. You won’t have to stress about higher premiums when you get older and possibly experience health issues. Talk to one of our brokers about the best available policies for you.

A beneficiary is a person listed on your life insurance policy which is the full or partial recipient of the death benefit provided by the policy. Anyone can be a beneficiary, and there can be multiple beneficiaries on the same plan. Note: No one is automatically listed as a beneficiary, including your spouse and children, so be sure to indicate your beneficiary choice(s) at the time of your policy purchase.

We are a fully transparent agency, there are no secrets or surprises. We allow consumers to see the companies we represent and allow them to quote prices before they contact us. We want them to know which company offers the lowest prices as opposed to us telling them. Once a program is selected by the consumer or suggested by TopLine, our clients are amazed at the speed in which they are approved for coverage. We have a family mentality that is productive and fun. Our office has almost no turnover, which means you get to know us very well. We are an insurance family, and we treat our clients as an extension of our family, without them, there is no TopLine Insurance.

Compare Quotes

Compare QuotesAt TopLine, we partner with some of the most reputable life insurance companies in the country. We can help you compare quotes and find the best deal.

Get Expert Advice

Get Expert AdviceOur life insurance brokers are experienced and passionate about finding the best policies for our clients. If you are unsure about your options or have any questions, they are happy to help.

Instant Approval

Instant ApprovalDon’t worry about medical exams or your financial situation. With TopLine, you can get approved for a life insurance policy instantly.

See What Our Clients Say

See What Our Clients Say

They said the application process would be fast. I was thinking I would be approved in a few weeks but somehow, they made sure we got approved the same day. Tracy made the approval process simple and walked me through everything.

- Tanya F.